Early planning by tourism businesses helped to prepare for a successful 2022 season.

Early in 2022, despite the concerns of the new Omicron variant and an especially slow start to the season, we were optimistic of a strong recovery in travel for the 2022 summer season. Our optimism was based on our belief of strong pent-up demand in three key markets; domestic leisure visitation, visiting friends and relatives, and our conventions and events market.

This understanding, along with the scenario planning work we undertook in partnership with the MacEachen Insititue in 2021, led us to advocate for the industry to “get ready” for what we believed would be a strong and rapid recovery in demand. We were encouraged and grateful to see many businesses respond to this call. In contrast to many other Canadian destinations, businesses in HRM started their hiring processes early, they committed to the return of live performances, and rather than adopting a “wait and see” approach, they started preparing early.

Likewise, in our own operations we committed additional investment in our key programs. We doubled down on our investment in marketing with new campaigns added to include Ontario, Alberta, and Newfoundland, and we increased our investments in conference and events sales activities. While many of our campaigns are still in market today, we are delighted to report tremendous success across all of our key performance measures. In particular, visitation to our destination’s website from our newly added markets of Alberta grew by 308%, Ontario 180%, and from Newfoundland at 329% as compared to pre-pandemic levels. Our traditional regional markets comprising the Maritime Provinces also grew by 18%, compared to pre-pandemic levels.

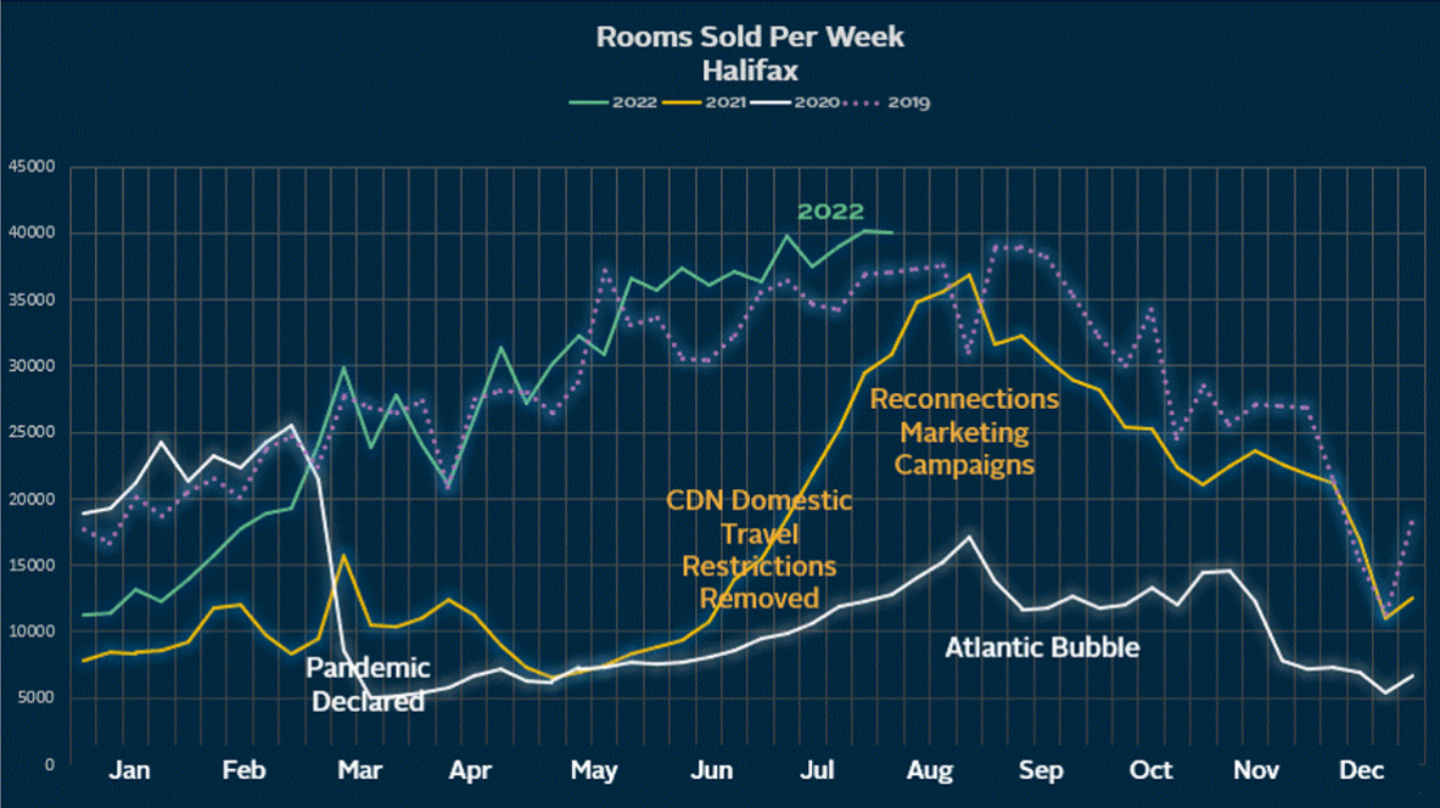

With the majority of the summer season now behind us, we are delighted to report that total rooms sold in HRM have now exceeded not only pre-pandemic levels but reached new all-time records with June and July sales at 15% and 13% higher respectfully. Halifax has also outperformed our Canadian competitive set for % of growth rooms sold YTD compared to pre-pandemic (with one exception of St. John’s). The average decline of the competitive set was 15% down from pre-pandemic levels.

While demand has returned this year, we know there are many real challenges remaining in our recovery particularly in labor availability, inflation, and supply chain challenges. As your DMO, we remain committed to working with you on both demand and supply side opportunities and challenges.

In closing, we want to express our gratitude to HRM and ACOA for their financial support, as our primary revenue source from the accommodations tax virtually disappeared in 2020 and 2021. We also want to recognize the strong partnerships with Tourism Nova Scotia and Destination Canada that helped extend our planned marketing programs.

Finally, we want to especially thank all of you who took a risk with us and invested early in getting ready for this summer. Without these investments, we would not have had the inventory of rooms to welcome guests, the capacity to serve visitors in restaurants, and we certainly would not have had the quality of experiences and vibrancy we all witnessed throughout HRM this past summer.